Taxes and Financial Planning for High Earners

How to Protect and Grow Your Wealth

Earning a high income in the United States creates opportunity—but it also creates complexity. As income rises, taxes become one of the largest expenses high earners face, often surpassing housing or lifestyle costs. Without proactive planning, a significant portion of your earnings can disappear to federal, state, and local taxes.

Effective tax planning isn’t about loopholes or aggressive tactics. It’s about using the tax code strategically and legally to keep more of what you earn and align your money with long-term goals.

In this article, you’ll learn:

- Tax strategies commonly used by high-income households

- How to reduce taxable income legally

- Advanced retirement contribution strategies

- Common tax planning mistakes high earners make

💼 Tax Strategies for High-Income Households

Why high earners need a strategy

High-income households often face:

- Higher federal marginal tax brackets

- Additional Medicare surtaxes

- State and local income taxes

- Phaseouts of deductions and credits

Without planning, it’s easy to overpay simply by default.

Common strategies used by high earners:

Maximizing tax-advantaged accounts

- Timing income and deductions

- Using pre-tax benefits effectively

- Coordinating investment and tax strategies

- Working with CPAs or financial planners

👉 The goal isn’t just tax reduction—it’s tax efficiency over time.

💰 Reducing Taxable Income Legally

High earners often focus on increasing income but overlook how much flexibility they still have to reduce taxable income.

Also check out: Taxes and Financial Planning for High Earners

Common legal strategies:

Pre-tax retirement contributions

Health Savings Accounts (HSAs) if eligible

Flexible Spending Accounts (FSAs)

Charitable giving strategies

Tax-loss harvesting in investment portfolios

Charitable giving strategies

Instead of donating cash annually, some high earners use:

Donor-advised funds (DAFs)

Bundling charitable contributions into high-income years

This allows for larger deductions while spreading out actual donations over time.

👉 Reducing taxable income doesn’t mean reducing lifestyle—it means redirecting money intentionally.

🧓 Advanced Retirement Contributions

Many high earners max out standard retirement options early—but additional strategies may still be available.

Beyond basic retirement accounts:

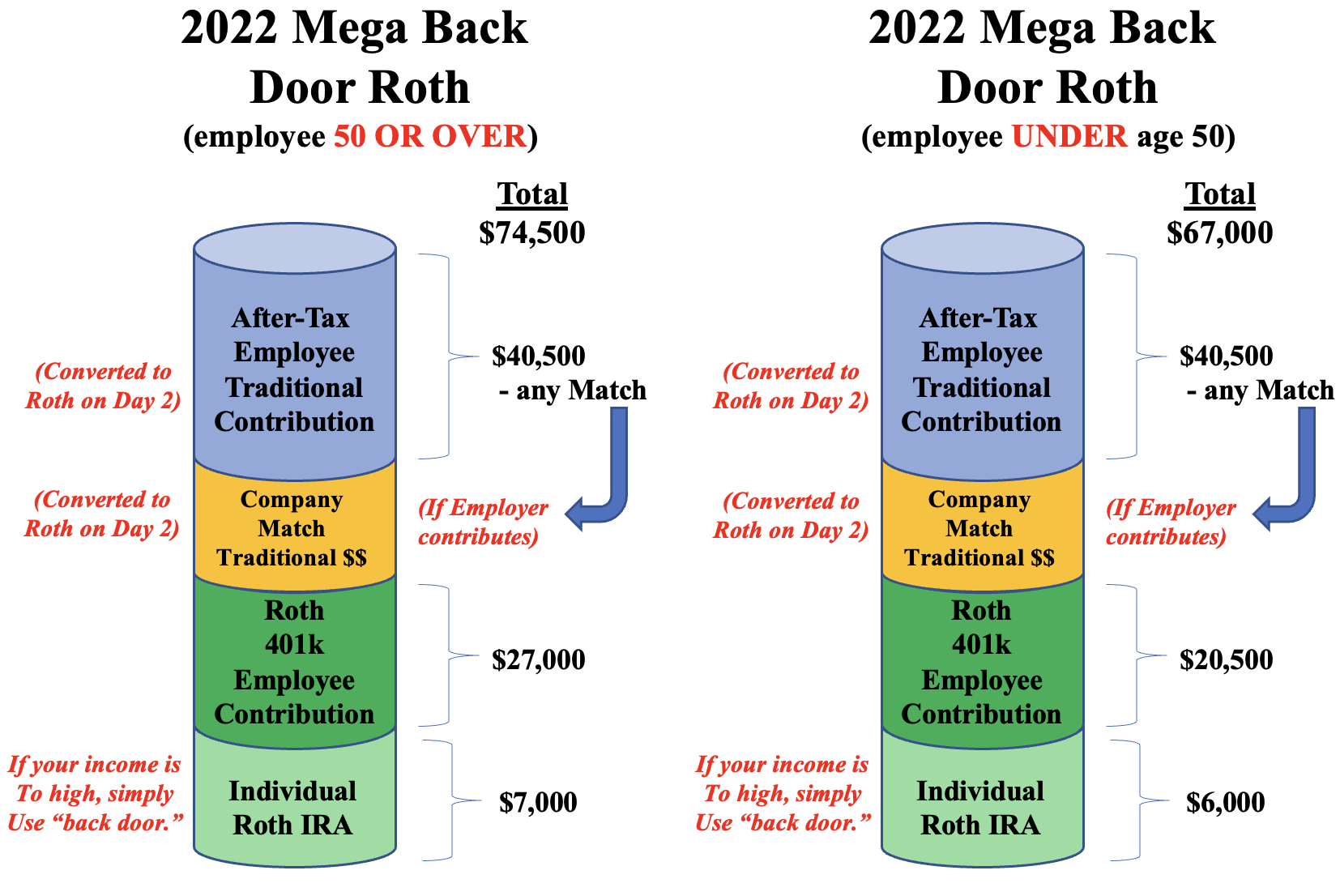

Backdoor Roth IRA – Allows Roth contributions despite income limits

Mega Backdoor Roth – Uses after-tax 401(k) contributions (if allowed by your plan)

Deferred compensation plans – Often available to executives

Solo 401(k) or SEP IRA for business owners

Why this matters

Advanced retirement strategies can:

Reduce current taxable income

Create tax-free income in retirement

Improve long-term compounding

👉 Retirement planning for high earners is less about access and more about optimization.

⚠️ Common Tax Planning Mistakes High Earners Make

Ironically, high earners often make costly tax mistakes—not from lack of income, but from lack of coordination.

Frequent mistakes include:

❌ Focusing only on income growth, not tax efficiency

❌ Ignoring state and local tax exposure

❌ Missing phaseouts and surtaxes

❌ Overconcentrating investments in taxable accounts

❌ Failing to plan charitable giving strategically

❌ Waiting until tax season instead of planning year-round

👉 Tax planning is proactive, not reactive.

📊 Coordinating Taxes With Financial Planning

Taxes should never be planned in isolation. The most effective strategies integrate:

-

Investment planning

-

Retirement goals

-

Estate planning

-

Cash flow management

For example:

-

A tax-efficient investment strategy can outperform a tax-inefficient one—even with lower gross returns

-

Strategic Roth conversions may reduce lifetime tax liability

-

Coordinating income timing can smooth tax brackets across years

👉 High-income financial success depends on coordination, not complexity.

🧠 The Mindset Shift High Earners Need

As income rises, the focus should gradually shift:

-

From earning more → to keeping more

-

From short-term savings → to long-term optimization

-

From tax minimization → to lifetime tax efficiency

This mindset shift often marks the difference between high income and true wealth.

✅ Final Thoughts

High income creates opportunity—but without smart tax planning, it also creates inefficiency. By understanding tax strategies available to high earners, reducing taxable income legally, using advanced retirement contributions, and avoiding common mistakes, you can significantly improve long-term outcomes.

Taxes are one of the few financial variables you can actively influence—but only if you plan ahead.

For high earners, financial success isn’t just about what you make. It’s about what you keep, grow, and protect.