Credit Score Secrets: How to Reach 800+ Faster

If you live in the United States, your credit score quietly influences some of the biggest decisions in your life: whether you get approved for an apartment, the interest rate on your car loan, how much you pay for a mortgage, and sometimes even your insurance premiums. That’s why the idea of reaching an 800+ credit score feels like unlocking a cheat code.

But an 800 score isn’t reserved for the rich or financially “perfect.” It’s usually the result of a handful of behaviors done consistently — and a few tactical moves most people never learn.

This guide breaks down what matters most in the FICO model, the lesser-known tricks that can move the needle, and realistic expectations for how long it takes to climb into the 800s.

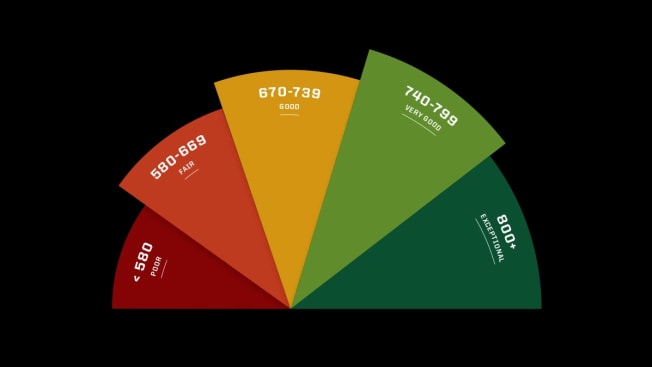

What an 800+ Credit Score Really Means

Generally, a score above 800 is considered “exceptional.” It signals to lenders that you’re low-risk: you pay on time, you don’t rely heavily on credit, and you’ve proven responsible use over time. The good news is you don’t need a massive income to get there — you need a strong profile.

Think of a credit score less like a grade on how “rich” you are, and more like a reliability score based on how you manage borrowed money.

The FICO Factors That Matter Most

FICO scores are calculated using several categories. While the exact algorithm is proprietary, FICO publicly shares the general weighting of each factor.

1) Payment History (Largest Impact)

Your payment history is the biggest contributor. One late payment can hurt for a long time, especially if your credit file is thin.

- Always pay at least the minimum on time (100% of the time).

- Set autopay for minimum payments even if you plan to pay in full manually.

- If you miss a payment, catching it within 30 days can sometimes prevent reporting (depends on the lender).

2) Credit Utilization (Fastest Lever to Pull)

Utilization is how much of your available revolving credit you’re using. It’s typically calculated per card and across all cards.

Targets that often correlate with higher scores:

- Under 30% is good.

- Under 10% is better.

- Under 3% is where many 800+ profiles live.

Important: utilization has no “memory” in most scoring models — it can improve quickly once reported balances drop.

3) Length of Credit History

The longer you’ve responsibly managed credit, the better. This includes:

- Age of your oldest account

- Average age of all accounts

This is why closing old cards can hurt — not always, but often.

4) Credit Mix

FICO likes to see you can manage different types of credit, such as:

- Revolving credit (credit cards)

- Installment loans (student loans, auto loans, mortgages)

You don’t need every type of loan. Never take debt just to “build credit.” But having a healthy mix can help.

5) New Credit (Hard Inquiries & New Accounts)

Applying for multiple accounts in a short period can lower your score temporarily. Hard inquiries and new accounts reduce your average age and can signal risk.

Rule of thumb: space out applications, especially if you’re preparing for a mortgage within the next 6–12 months.

Less-Known Tricks to Reach 800+ Faster

Pay Twice Per Month (Or Before the Statement Closes)

Many people pay the bill by the due date and still see high utilization because the balance reported to bureaus is usually the statement balance, not what you owe after payment.

Tactical move: pay down your card before the statement closing date so the reported balance stays low.

Use “All Zero Except One” (AZEO)

AZEO is a strategy where you let one card report a small balance (for example 1–3% utilization) and have all other cards report $0.

This can be especially useful 30–60 days before applying for major credit (like a mortgage), because it optimizes utilization without requiring new accounts.

Ask for Credit Limit Increases (Without More Spending)

A higher total credit limit can reduce your utilization ratio instantly — as long as your spending stays the same.

- Request increases every 6–12 months (issuer-dependent).

- Some issuers do a soft pull; others may do a hard inquiry.

- Even one increase can significantly improve your utilization profile.

Keep Old Accounts Open (If They’re Free)

If you have a no-annual-fee card, keeping it open can help maintain a longer credit history and more available credit. If the card has an annual fee and you don’t use it, consider downgrading instead of closing.

Become an Authorized User (If Done Carefully)

Being added as an authorized user on someone’s long-standing, low-utilization card can sometimes boost your score by adding their account history to your report.

Important: this only works if the primary cardholder has excellent habits. If they miss payments or carry high balances, it can backfire.

Dispute Real Errors, Not Legitimate Debt

Check your reports for inaccuracies: wrong balances, accounts you don’t recognize, incorrect late payments, or duplicate accounts. Fixing legitimate errors can lead to faster improvements than any “hack.”

How Long Does It Take to Reach 800+?

This depends on where you’re starting and what’s holding your score back. Here are realistic ranges:

If Your Main Issue Is High Utilization

Potential timeline: 1–2 months after your lower balances are reported. This is one of the quickest score improvements you can make.

If You Have Limited Credit History

Potential timeline: 6–24+ months. Time is the key ingredient here. You can optimize utilization and payments, but you can’t instantly create years of history.

If You Have Late Payments or Derogatory Marks

Potential timeline: 12–36+ months for meaningful recovery, depending on severity and recency. Positive behavior over time reduces the impact, but serious negatives can take years to fade.

Also check out: Build Wealth in Your 20s (Even With Student Loans)

A Practical 30-Day Action Plan

- Set autopay for minimum payments on all accounts.

- Pay down credit cards to under 10% utilization (ideally under 3%).

- Make payments before statement closing dates.

- Request a credit limit increase (if likely to be a soft pull).

- Check credit reports for errors and dispute inaccuracies.

Frequently Asked Questions (FAQ)

What’s the fastest way to increase my credit score?

For many people, the fastest improvement comes from lowering credit card utilization. Paying balances down before statement closing dates can move your score within one or two reporting cycles.

Is it possible to get an 800 credit score without a mortgage?

Yes. While a mortgage can contribute to credit mix and long history, many people reach 800+ with credit cards and installment loans (like student or auto loans), as long as utilization stays low and payments are always on time.

Does carrying a balance help your score?

No. You don’t need to carry debt to build credit. What helps is having a card report a small balance (even $5–$20) and then paying it off in full by the due date. Interest is optional; good reporting is not.

How many credit cards do I need for an 800 score?

There’s no magic number, but having multiple cards can help keep utilization low and strengthen your profile. Many 800+ profiles have 3–5 cards, but fewer can work if managed well.

Why did my score drop after I paid off a loan?

Paying off an installment loan can sometimes lower your score temporarily because it changes your credit mix or reduces the number of active accounts. This is usually short-term and not a sign you made a bad financial decision.

Conclusion

Reaching an 800+ credit score isn’t about secret loopholes — it’s about mastering a few high-impact levers and using them consistently. Focus first on perfect payment history and low utilization, because those two areas typically drive the biggest improvements.

Then use tactical moves like paying before statement close, AZEO, and strategic credit limit increases to accelerate results. Finally, be patient with the part you can’t hack: time. A long, clean credit history is one of the strongest signals to lenders, and it builds month by month.

If you want an 800+ score faster, aim for a profile that looks boring: low balances, on-time payments, and long-standing accounts. In credit scoring, boring is powerful.